manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

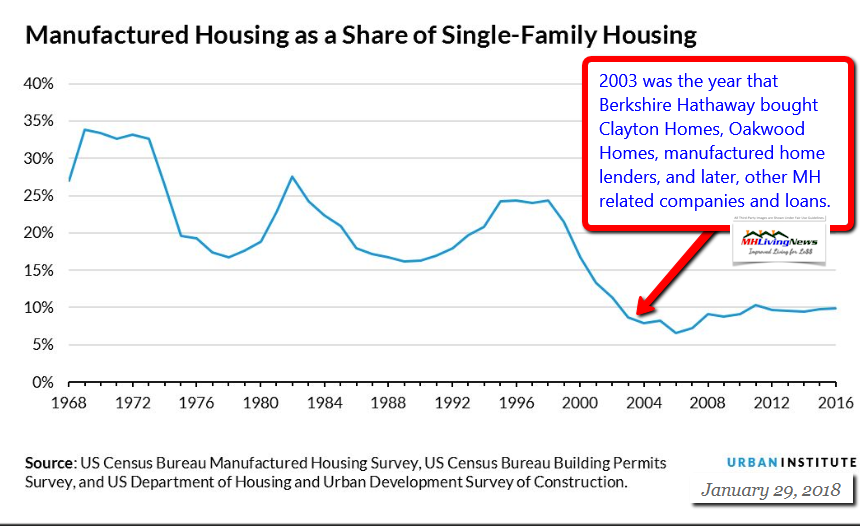

“During my time at MHI, I was often asked the same question, “What must happen for business to return – for manufactured housing to begin growing again? ” My stock answer would usually start with ‘financing’ and end with a general comment about the need to bring ‘value’ to our customers.”

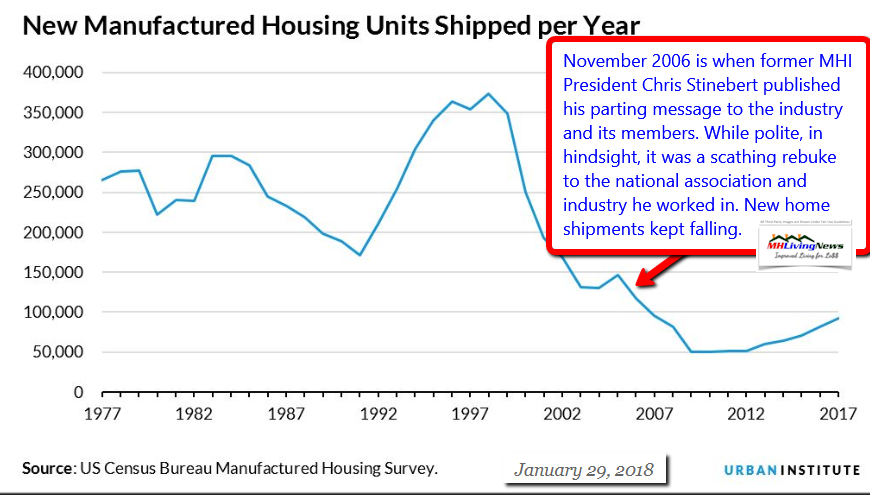

The person making that comment was Chris Stinebert. It was his departing message as the president of the Manufactured Housing Institute (MHI) to the manufactured home industry at large. It was published in the now-defunct Journal of Manufactured and Modular Housing.

Why review this now?

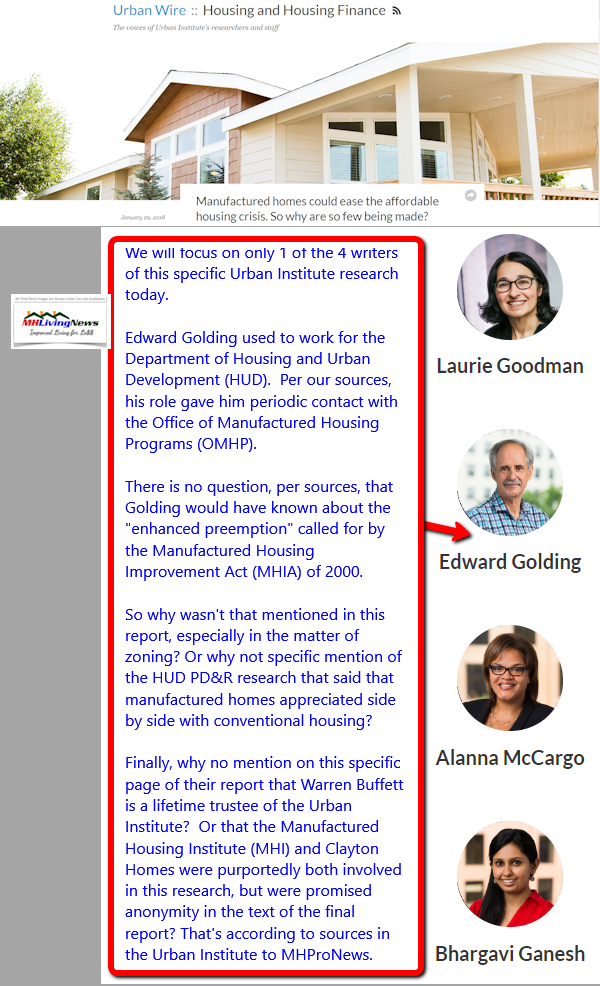

That will become ever more apparent as this article evolves. But the short answer is that almost a year ago, the Urban Institute (UI) said this: “Manufactured homes could ease the affordable housing crisis. So why are so few being made?” They asked an intelligent question, made a case for why more manufactured homes would be good, and developed some useful points. But UI arguably missed other important elements entirely. Some of those missed points by UI are better understood when MHI’s former president’s thoughts are explored and more fully grasped.

Both Stinebert’s and Urban Institute items will be considered in this analysis. Let’s continue with MHI’s former president’s first point. Note, that on the first or some other points he made, we are neither agreeing nor disagreeing, merely sharing precisely what MHI’s former president said.

“1. Manufacturers would step up and take control of the marketplace. This means setting strict requirements for their retailers, including the appearance of the sales center, acceptable business practices and ethics. Then, manufacturers need to enforce these requirements. For far too long, manufacturers have served as ‘enablers, ” permitting retailers to continue their faulty practices, lowering the bar for all competing retailers, and perpetuating a negative image for our industry with potential customers. Retailer excellence, not volume, needs to be rewarded and questionable business practices should bring severe consequences.”

“2. Manufacturers should assume the responsibility for customer satisfaction. Why? Because no one else is capable of performing this task on a consistent, reliable basis. And it is a task that must, absolutely must, be performed. As various market research projects have told us, better customer satisfaction is critical to improving the appeal of manufactured housing to new homebuyers. Without better customer service, this industry will remain a boutique, cottage industry mired forever in the 120, 000 annual production range. This means is that each manufacturer would to be responsible for the placement of the home and anything else that needs to be repaired during the warranty period.”

We’ll briefly note that the above has pros and cons, the larger firms could do this more easily, smaller ones, this might be a barrier to stay in the industry, if it were mandated.

“3. The industry needs to launch a national advertising offensive spotlighting the tremendous benefits of owning and living in a factory built home. The national campaign could focus on the quality of materials and construction; design and customization potential; speed of delivery; and product innovation. It’s time for the public to see positive images of factory-built homes, eliminate the myths, and begin laying the foundations for future growth. To the naysayer who might oppose a national campaign, I ask – if not now, when? And, if not us, who? There will never be a better or more appropriate time to launch an advertising offensive. We have the best homes on the market and it’s time the public was educated on this fact – it’s both our duty and responsibility.”

There is a case to be made that local marketing and education – that blankets the nation market-by-market – could be more effective. But note that the video of Kevin Clayton in our recent report linked below said 5 years after this was written by Stinebert that they were ready then to do just such a campaign as MHI’s departing president suggested. What happened? Why didn’t that campaign Clayton spoke about occur then?

“4. It’s also time for this industry to finally start sharing the risks and the rewards. Lenders, including new lenders, are much more likely to lend money to potential homeowners if the retailer and manufacturer are willing to share some of the risk. This “sharing” could take multiple forms, but the common thread running throughout the process must be the alignment of interests for a successful, performing loan.”

This was perhaps his weakest argument. How many conventional housing builders shares the risk in the loans made on the homes they sell? This most certainly was a flawed concept, however good the intention behind it may have been.

“5. Manufacturers and retailers should be more open about making pricing information more available to potential customers. It’s time to stagger out of the dark ages and discard the long held philosophy that “an educated consumer is manufactured housing worst customer. The information age is here and we better get used to it. Sticking our collective heads in the sand is not going to make it go away. The recent Foremost Insurance study showed that over 90 percent of manufactured homeowners have a computer. The National Association of Realtors and Yahoo reported that more than three- out- of- four homebuyers started their home search on the Internet and every one of these searches was launched by price range and geography. If this industry wants to continue ignoring three- out- of- four homebuyers, we deserve the consequences.”

Since this was published in November 2006, this remains an issue for many.

“6. Focus on the issues of real importance and stop looking to Washington to solve all of your problems. HUD, Fannie Mae and Freddie Mac did not cause your world to collapse and they are not going to be your salvation either. This is not to say these entities and Congress are not important…they are. But, all too often, we lose our perspective by putting excessive emphasis on Washington and ignoring the major issues impacting our declining market share. (See 1- 5 above!)”

This is another point that however well intended, is arguably weak and flawed, starting with its premise. Imagine if conventional housing suddenly had HUD – which overseas FHA loans – Fannie Mae and Freddie Mac all pulled their lending from conventional housing? “The federal government now invests or insures over 90 percent of mortgages in the US via Fannie Mae, Freddie Mac and Ginnie Mae.” According to Penny Mac USA on Jul 20, 2017. “Ginnie Mae is the government agency that issues mortgage bonds backed by Federal Housing Administration or Department of Veterans Affairs loans, among others,” notes Housing Wire. So it is arguably misguided at best to think that if 90 percent of conventional housing mortgages need this support, why shouldn’t manufactured homes get that same support – and on part with conventional housing? More on this in a few moments, further below.

That said, Stinebert’s point reflects the incredible importance to the marketplace for manufactured housing – or all housing – of credit. The reason that housing prices fell like a rock in the aftermath of the 2008 mortgage credit crisis is precisely because due to the high price, buying or selling a home needs financing.

“7. Stop tilting after windmills…go after those things that can be realistically achieved. Yes, if I the HUD Code were being written today, there would be no need to require a permanent chassis to stay with a HUD-Code home. The chassis issue is a vestige of an earlier industry dealing with limited abilities and techniques. But attempting to remove the chassis requirement through Federal legislation might prove politically implausible, with too many strong and formidable opponents who will fight to preserve the status quo. ‘We don’t need to become like Don Quixote tilting after windmills – fighting battles that cannot be won.

Instead, we should aggressively pursue meaningful and realistic changes to the HUD Code that would free the manufactured housing industry to) design/build innovative homes, such as two-story homes, stair architecture, single-family attached and other non-traditional designs. Such a strategy would certainly be achievable and, if accomplished, would be a tremendous step forward for manufactured housing.”

This section is arguably a mixed bag of accurate, misleading, perhaps uninformed, and thoughtful commentary by Stinebert. For example, did he know that it was MHI in the 1990s who reportedly foiled the adoption of an amendment offer by Indiana Representative John “Jack” Hiler (IN3-R), that would have made chassis removeable? That’s according to a former MHI vice president to MHLivingNews.

This section is arguably a mixed bag of accurate, misleading, perhaps uninformed, and thoughtful commentary by Stinebert. For example, did he know that it was MHI in the 1990s who reportedly foiled the adoption of an amendment offer by Indiana Representative John “Jack” Hiler (IN3-R), that would have made chassis removeable? That’s according to a former MHI vice president to MHLivingNews.

The balance of Stinebert’s comments on point 7 above have some merit, but a removable chassis – in the era of “green” and “recycling” – is an idea that is long overdue. Especially, as the affordable housing crisis continues to grow.

Stinebert concluded his parting message with this thought.

“8. The entire industry must focus on one goal – increasing the value proposition to the homeowner. If we cannot offer our homeowners realistic value for their housing dollar, how do we expect to compete in the marketplace. This means giving the customer true value with their purchase, then keeping them happy after the sale. This means insuring the homeowner builds equity and wealth in their home. And finally, this means providing for stable, viable resale market for when it is time to sell the home. Once the industry delivers this value, the rest will fall into place naturally.

Again, these issues are a compilation of my “wish list” for manufactured and modular housing. A future that I truly believe is filled with tremendous promise and hope. I remain firmly convinced that factory-built housing will one day exceed all expectations – dreams will become reality – but only if a united industry is willing to take the necessary steps – and pay the price for change. (See 1- B above)”

Once more this is a mixed bag, as “a united industry” is MHI talk, arguably designed to silence other voices such as the Manufactured Housing Association for Regulatory Reform (MHARR). It was ARR – the prior name for MHARR – that had worked for the adoption of Hiler amendment at the cusp of adoption as part of a large housing bill circa 1990 – which MHI late pulled out of supporting. A HUD spokesperson told MHProNews last year that HUD has no expectation of industry unity, and that it is unrealistic to expect it.

Another point that could be objected to is that the industry had already shown its value in the marketplace for decades. But that may be a literary device, not meant to be taken literally. Absent from this list by Stinebert is any mention of “enhanced preemption,” made law by the Manufactured Housing Improvement Act of 2000. More on that in a linked related report, below the by line and notices.

Some various concerns noted, the above by Steinbert nevertheless has several salient points to our time, and the review of the Urban Institute report from January 29, 2018. Among them?

- Stinebert’s comments about the resale market – that’s a telling point. And he is correct in saying there is linkage between wealth building – equity building – and financing.

- His points about educating the public can’t be overlooked. Who’s fault was it that the public wasn’t being educated? Wasn’t MHI the largest association? Didn’t they claim to represent all aspects of manufactured, modular and factory-built housing?

- Stinebert’s emphasis on financing, the value proposition to consumers at large, existing customers, and education are all areas that MHI has obviously failed at, or why did he feel the need to mention them at all?

- Why did Chris wait until he left to produce this list? Was it in some respects a kind of polite backhanded slap at MHI?

With these points made, and salient questions raised, a few thoughts from the Urban Institute, almost a year later.

The video posted is a useful reference from an unpaid affordable housing focus group. The focus group members were given a meal and gas money only, to talk about their experiences with modern manufactured homes. Almost everyone in this video owned a conventional house first. It goes to some of the points that Stinebert, UI, and others have made.

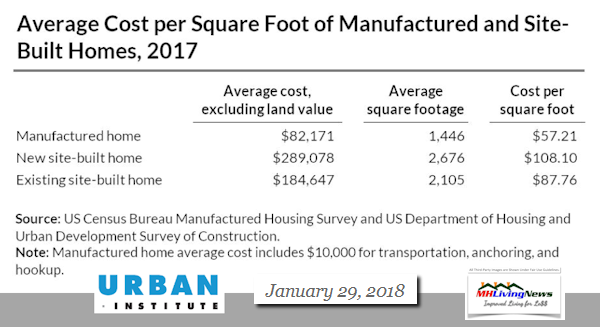

Urban Institute’s January 29, 2018 Research Report

What Stinebert’s parting words – or parting shots? – reveal, especially in the light of what the Urban Institute noted, is important to:

- manufactured home owners,

- affordable housing seekers and advocates,

- manufactured housing industry professionals and investors,

- plus public officials, investigators, and arguably plaintiffs’ attorneys too.

More lending means higher resale values.

More lending means more competition, and lower rates of financing rates than the Berkshire Hathaway backed lenders often offer.

More public education would mean more demand. That – coupled with the other factors cited above – would mean higher resale values.

Put differently, when the facts are interlocked like jigsaw puzzle-pieces, an image begins to emerge. That image is one where MHI has failed not only the bulk of its own industry professionals, but also tens of millions of current and potential manufactured home owners too.

A former MHI vice president told MHLivingNews today – as this article was being prepared – that the corruption at MHI runs deep and long. It predates the current regime there. We will explore that more in the days ahead. In the meantime, check out the related reports, linked further below.

In closing, these data points and quotes – as vexing as they are – shouldn’t deter someone from a manufactured home. Quite the opposite. They help explain why so relatively few are being sold. The value is there, as Stinebert, the Urban Institute, the National Association of Realtors™ (NAR), third-party researchers for HUD and others have documented.

These points should also spark further investigations into why the solution to affordable housing has been sidetracked, at the very time when tens of millions of Americans need it the most. “We Provide, You Decide.” © ## (Lifestyle news, commentary, and analysis.)

(Third-party images and citations are provided under fair use guidelines.)

Soheyla Kovach co-founder of MHLivingNews, on left,

with son Tamas (pronounced like Tah Mash), and publisher L. A. ‘Tony’ Kovach, on the right.

Related Reports:

FEAR, a Solution to the Affordable Housing Crisis, and the Manufactured Home Dilemma

Compelling Information for Renters and Manufactured Home Owners