manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

Senators, CFPB Chief Richard Cordray Explain How Current Rules Harm

Manufactured Home Owners, Buyers, Sellers and Lenders in the Under-$100K Market

For the past year or so, various media outlets have framed unflattering stories about manufactured housing around the premise that the industry’s lending practices unfairly gouge people of modest means, and that Dodd-Frank regulations have failed to protect them.

But during that time, in a parallel universe, lawmakers and regulators have engaged in earnest discussions that support an entirely different conclusion: The misguided implementation of this well-meaning legislation is hurting buyers, sellers and lenders in this critical market for affordable housing.

This video report, featuring testimony available in its entirety to anyone who wants to tune in to C-SPAN, suggests that business and financial reporters might want to re-think past stories on this issue and set the record straight.

Here, Richard Cordray, director of the Consumer Financial Protection Bureau — the agency that oversees the Dodd-Frank rules — discusses before two Senate committees:

- Why, percentage-wise, there are higher costs for originating and servicing conventional housing and manufactured home loans under $100,000

- How Dodd-Frank allowed for that reality, and gave the CFPB rule-making authority to adjust the points/fees/costs, so as not to choke off credit access to consumers, and

- That “there never was much high-cost lending” on manufactured housing loans — a point that refutes the very foundation of news stories that accuse MH industry lenders of gouging customers.

During one hearing last spring, Sen. Richard Corker (R-Tenn.) points out that the current rules have become obstacles in the path to home ownership, and that some people are paying more to rent homes than they would to own them.

Cordray agrees that this “isn’t optimal for anyone.”

In the most recent hearing, Sen. Joe Donnelly (D-Ind.) spoke at length about the negative impact on MH lending, due to the CFPB’s regulations.

You’ll hear from a professional couple who told MHLivingNews how these regulations created numerous obstacles in their quest to finance their upscale retirement home.

There is additional information that financial writers might want to consider in reporting this issue.

In a separate video linked here, a manufactured home lender explains that with no federal subsidies and with no taxpayer risk, manufactured home personal property loans — known as chattel or home-only financing — are made at the lender’s risk.

If there was a way for other lenders to charge less and still profit, he says, they would enter the market and could rapidly dominate. The fact that they don’t, suggests that manufactured home lending is not by any means predatory.

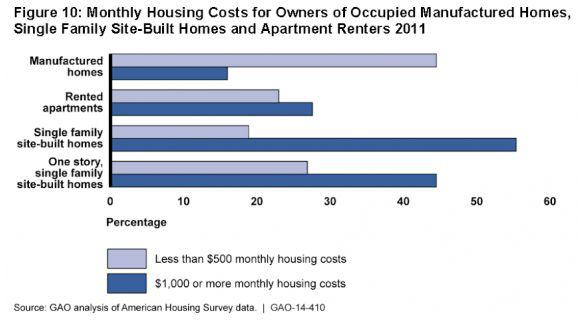

A 2014 GAO report on manufactured home lending shows that even with a modestly higher rate – due to the factors that Richard Cordray and the lender linked above explain – the actual monthly payment on manufactured homes is lower, on average, than any other kind of housing option.

In recent years, the bulk of in depth news reports on the actual impact of federal regulations on lending have been originated by MHLivingNews.com and MHProNews.com. Regrettably, media accounts like The Seattle Times/Center for Public Integrity/Buzz Feed and The PBS NewsHour are riddled with misleading or inaccurate information.

With the affordable housing crisis growing, there is an urgent need for fresh, accurate reporting that shines a light on the unfortunate consequences of federal rules that were well intended, but instead hurt the very people they were meant to help. ##

Editor’s Note: Click the images and links above for additional reports on this topic.

By L. A. ‘Tony’ Kovach.